Introduction

Financial institutions are among the most targeted organizations in any sector. According to the 2025 Verizon Data Breach Investigations Report, the financial and insurance sector recorded 3,336 incidents and 927 confirmed breaches in a single year, with 90% driven by financial motives. The average breach cost hit $6.08 million in 2024, 22% above the global average.

Penetration testing gives organizations a way to find those vulnerabilities first. Certified ethical hackers simulate real-world attacks against your systems, exposing gaps before actual threat actors can exploit them. For banks, credit unions, fintech platforms, and mortgage brokers, this is no longer optional; GLBA, FFIEC guidelines, and PCI DSS each carry explicit testing mandates.

This guide covers what compliance officers, CISOs, and IT leaders need to know: which regulations require testing, which testing types fit different scenarios, how a quality engagement runs, and how findings build a stronger, audit-ready security posture.

Key Takeaways

- Penetration testing is explicitly required under GLBA (annually), FFIEC (risk-based frequency), and PCI DSS (Requirement 11.4)

- Financial institutions face expanded attack surfaces: online banking, mobile apps, APIs, and third-party integrations all require active testing

- Black box, white box, and gray box testing each serve distinct compliance and operational purposes; choose based on what you're trying to prove

- A quality engagement follows five phases: planning, reconnaissance, scanning, exploitation, and reporting

- Findings must be prioritized, remediated, and retested; the report is the beginning, not the end

Why Financial Institutions Are Prime Targets

Financial institutions hold the most monetizable data on earth. Account credentials, transaction histories, credit profiles, and personally identifiable information can be sold, exploited for fraud, or held for ransomware payments. The Verizon 2025 DBIR confirms that personal data appeared in 54% of financial sector breaches, credentials in 22%, and ransomware in 44% of all breaches across industries.

Beyond data value, attackers hold reputational leverage. A publicized breach creates regulatory scrutiny, customer attrition, litigation exposure, and lasting damage to brand trust, pressure that increases the likelihood an institution pays to make an incident go away quickly.

The Expanding Attack Surface

Digital transformation has multiplied the entry points available to attackers. Every new channel introduces new risk:

- Online and mobile banking portals: authentication flows, session management, and account access controls

- Open banking APIs and third-party integrations: partner connections that often receive less security attention than core systems

- Payment gateways: transaction integrity, encryption, and fraud detection bypass opportunities

- Cloud-hosted platforms: IAM misconfigurations, data segregation gaps, and privilege escalation paths

Application-layer DDoS attacks against financial services increased 23% from 2023 to 2024, according to FS-ISAC and Akamai, a direct reflection of how exposed the sector's web-facing infrastructure has become.

Proactive vs. Reactive Security

Each of those attack vectors requires active verification, not assumptions. Reactive security means absorbing damage after a breach has already occurred. Penetration testing changes that posture.

A well-executed test surfaces more than technical vulnerabilities. It exposes gaps in business logic, weaknesses in fraud controls, and blind spots in incident response, before an attacker confirms them first. For financial institutions, finding those gaps internally is far cheaper than discovering them through a regulatory enforcement action or a client-facing incident.

Regulatory Requirements Mandating Penetration Testing

Each regulation below carries distinct testing requirements, scope definitions, and independence standards. Getting this right means understanding what each framework actually demands, not just checking a box.

GLBA Safeguards Rule (16 CFR § 314.4(d)(2))

This is the most explicit federal mandate. The updated Safeguards Rule, finalized in December 2021, requires financial institutions to either implement continuous monitoring or conduct annual penetration testing plus vulnerability assessments at least every six months (and after any material system changes).

GLBA's reach extends well beyond banks. Mortgage brokers, auto dealers offering financing, financial advisors, and tax preparers all fall under this requirement. The FTC examines whether testing programs satisfy the rule's substance, not just whether a report exists. Impact Risk Advisors structures pen test cadences specifically to meet that standard for non-bank financial entities.

FDIC and FFIEC Guidelines

Under 12 CFR Part 364 Appendix B, financial institutions must "regularly test the key controls, systems, and procedures" of their information security programs, with frequency driven by risk assessment. Critically, tests must be conducted or reviewed by independent third parties or independent staff, meaning the people who built or operate the system cannot be the ones testing it.

The FFIEC IT Handbook (Sections IV.A.2–IV.A.4) goes further, calling for:

- Tests that simulate real-world attacks selected by experienced testers

- Independent testers with no operational responsibility for tested systems

- Prioritized findings with remediation options and repeat-issue tracking

- Pre-launch testing for new or significantly changed external-facing applications

PCI DSS v4.0.1

Under the current standard (v4.0.1, June 2024), Requirement 11.4 governs penetration testing. Requirement 11.4.4 is unambiguous: exploitable vulnerabilities found during pen testing must be corrected, and testing must be repeated to verify the fixes. Requirement 6.3.3 sets a one-month window for critical and high-severity patches. This applies to any institution handling cardholder data.

SOX Section 404

SOX doesn't explicitly name penetration testing, but Section 404 requires management to assess the effectiveness of internal controls over financial reporting (ICFR). Most financial institutions have IT systems directly in scope for that assessment. Penetration testing provides documented evidence that those systems resist unauthorized access or manipulation, supporting IT general controls (ITGCs) rather than serving as a standalone SOX requirement.

The Cost of Non-Compliance

Failing to meet testing requirements carries real consequences: regulatory findings during examinations, civil money penalties, and weakened standing with cyber insurers. The OCC levied an $80 million penalty against Capital One following cybersecurity risk management failures. That figure represents a tangible benchmark, and a reminder that examiners treat testing gaps as control failures, not paperwork oversights.

Types of Penetration Testing Used in Financial Services

Black Box, White Box, and Gray Box Testing

| Testing Type | Tester Knowledge | Best Used For |

|---|---|---|

| Black Box | None, simulates an external attacker | External threat simulation, realistic attack scenarios |

| White Box | Full access: source code, architecture, credentials | Validating internal controls, authenticated application testing |

| Gray Box | Partial: role-based access, limited system knowledge | Compliance-driven testing, API and partner integration testing |

For most compliance-focused financial institutions, gray box is the practical starting point; it mirrors how a partner, vendor, or authenticated user interacts with your systems. Where the concern is privilege escalation or unauthorized data access, white box testing provides the depth to validate those controls properly.

External, Internal, and Red Team Testing

- External testing: attacks internet-facing systems from outside the perimeter: web applications, VPNs, public APIs, DNS configurations

- Internal testing: simulates a threat that's already inside: compromised credentials, insider threat scenarios, lateral movement between systems

- Red team exercises: full-scope adversary simulation testing people, processes, and technology simultaneously; more resource-intensive but most realistic for mature programs

FFIEC guidance explicitly supports institutions in selecting testing type based on their own risk assessment; the right choice depends on your threat model, regulatory obligations, and program maturity.

Compliance-Driven vs. Risk-Based Testing

Compliance-only testing satisfies a regulatory checkbox: annual test, report delivered, box checked. Risk-based testing goes further: it prioritizes the most critical systems, increases frequency where exposure is highest, and feeds findings directly into the broader security program.

The gap matters. A point-in-time test scoped only to what regulators explicitly name can miss significant vulnerabilities in adjacent systems. Effective penetration testing for financial institutions reflects actual risk exposure, not just the minimum required to pass an examination.

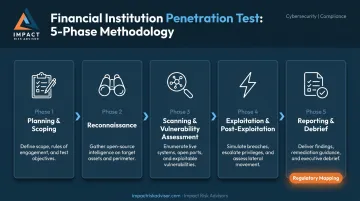

The Penetration Testing Methodology: Key Phases

Phase 1: Planning and Scoping

Scoping determines everything downstream. A well-defined scope should:

- Identify which systems, applications, and networks are in scope based on the institution's risk profile

- Establish rules of engagement between the testing team and internal stakeholders

- Schedule testing windows to avoid production disruption

- Document reporting requirements before work begins

Independence is non-negotiable. The FFIEC requires that testers not be responsible for the design, installation, maintenance, or operation of any system they test.

Phase 2: Reconnaissance

Testers gather intelligence before touching a single system:

- Passive: WHOIS lookups, DNS enumeration, public records, social media analysis, exposed credentials in public repositories

- Active: Network mapping, port scanning, service fingerprinting, subdomain enumeration

In financial services, even reconnaissance must be carefully timed. Active scanning can trigger security alerts in production systems; coordination with the institution's security team is essential.

Phase 3: Scanning and Vulnerability Assessment

Automated tools like Nessus and OpenVAS identify potential vulnerabilities across the target environment. Automated scans alone aren't enough, though. Every finding requires manual verification to eliminate false positives that would otherwise waste remediation cycles.

Common vulnerability classes in financial applications include:

- Authentication bypass and session management weaknesses

- SQL injection and other injection vulnerabilities

- Insecure direct object references (accessing other users' accounts or records)

- Cryptographic weaknesses in data at rest or in transit

Phase 4: Exploitation and Post-Exploitation

This phase answers the critical question: can an attacker actually reach financial data, or do the vulnerabilities just theoretically exist?

Testers demonstrate real-world impact by attempting:

- SQL injection against banking applications

- Authentication bypass and privilege escalation

- Lateral movement between connected systems

- Segmentation testing to determine how far a compromised system can reach

This is where the distinction between "vulnerability exists" and "vulnerability is exploitable" becomes concrete.

Phase 5: Reporting and Debrief

A complete pen test report for a financial institution should include:

- Executive summary: risk levels, business impact, compliance implications in non-technical language

- Technical findings: reproduction steps, evidence screenshots, affected systems, and CVSS scores

- Severity classifications: critical, high, medium, low, with clear criteria

- Regulatory mapping: findings tied to specific GLBA, FFIEC, PCI DSS, or NIST 800-53 requirements

- Prioritized remediation recommendations: what to fix first and why

Impact Risk Advisors includes compliance-mapped findings and prioritized remediation guidance in every engagement deliverable, so security teams can act on results immediately rather than translating technical output into regulatory context themselves.

What Financial Systems Should Be in Scope

Core Banking Applications and Customer Portals

Online banking platforms, loan origination systems, treasury tools, and internal employee dashboards all carry authentication risks, session hijacking exposure, and business logic vulnerabilities. Testing should specifically probe whether a user can manipulate transaction workflows, escalate their own account privileges, or access records belonging to other customers.

Payment Gateways and APIs

Payment systems require testing for transaction integrity (can payments be intercepted or replayed?), encryption of data in transit and at rest, and fraud detection bypass scenarios.

Financial APIs (powering mobile apps, open banking interfaces, and third-party integrations) should be assessed against the OWASP API Security Top 10, including Broken Object Level Authorization (API1:2023) and Broken Object Property Level Authorization (API3:2023).

Shadow and undocumented endpoints deserve specific attention: they're often the path of least resistance.

Cloud, Vendors, and Social Engineering

Three additional areas belong in scope for most institutions:

- Cloud environments: IAM role configurations, data segregation in SaaS platforms, and privilege escalation paths within AWS, Azure, or GCP deployments.

- Third-party vendors: OCC's 2023 interagency guidance sets clear expectations for third-party risk management. Vendor-hosted portals, fintech integrations, and API connections to partners should be in scope when they process or access institution data.

- Social engineering: FFIEC guidance increasingly expects institutions to evaluate human-factor vulnerabilities. Impact Risk Advisors includes phishing simulations and social engineering scenarios as part of full-scope financial services engagements, testing whether employees and processes hold up against manipulation-based attacks.

From Findings to Fixes: Remediation and Ongoing Compliance

Prioritize by Risk, Not Finding Count

A report with 47 findings is not a crisis if 40 of them are low-severity configuration issues. Prioritization requires assessing two dimensions:

- How much financial, regulatory, and reputational damage the vulnerability could cause

- How easily an attacker could exploit it given the access and complexity required

A critical vulnerability enabling remote code execution or direct exposure of customer financial data demands emergency response, not a scheduled patching cycle.

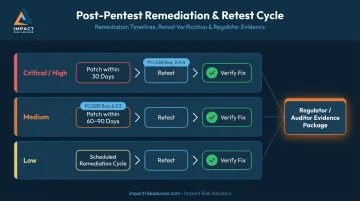

Remediation Timelines and Retesting

PCI DSS Requirement 6.3.3 requires critical and high-severity patches within one month of release. For other frameworks, timelines are institution-defined, but they must be defined, documented, and followed.

Remediation isn't complete until it's verified. PCI DSS Requirement 11.4.4 explicitly requires retesting after corrections. Most institutions conduct targeted retests within 30–90 days of initial report delivery, depending on finding severity and remediation complexity. Retesting evidence is what regulators, auditors, and cyber insurers actually want to see.

Building a Continuous Testing Program

The GLBA Safeguards Rule requires annual penetration testing at minimum. That's a floor, not a ceiling. FFIEC's emphasis on "continuous improvement" means test findings should feed into a repeating cycle, informing policy updates, architecture decisions, and security awareness programs, not sitting in a folder until the next examination.

Impact Risk Advisors' embedded approach integrates pen testing into a broader compliance program that runs year-round. Findings feed into a prioritized remediation action plan, vCISO oversight tracks progress through to resolution, and board-level reporting translates technical results into language that executives and examiners can act on, all within a six-phase continuous compliance model built to keep pace with an evolving threat landscape.

Frequently Asked Questions

What is the purpose of penetration testing in banks?

Penetration testing serves two purposes: proactively identifying exploitable vulnerabilities in systems, applications, and networks before attackers do, and fulfilling regulatory requirements under GLBA, FFIEC, and PCI DSS. It goes beyond vulnerability scanning by demonstrating actual exploitability and business impact.

What are the phases of a penetration test?

Standard phases include planning and scoping, reconnaissance, scanning and vulnerability assessment, exploitation and post-exploitation, and reporting with remediation guidance. The core sequence is consistent across frameworks like PTES and NIST SP 800-115.

How much does a financial institution penetration test cost?

Cost varies based on scope, environment complexity, testing type, and whether retesting is included. Contact Impact Risk Advisors directly for a scoped estimate based on your institution's specific environment.

Does NIST 800-53 require penetration testing?

NIST SP 800-53 Rev. 5 Control CA-8 explicitly requires penetration testing at organization-defined frequencies. Financial institutions commonly apply it as a supplemental framework alongside GLBA and FFIEC, especially federal regulators and government contractors.

What are the most common penetration testing techniques in financial services?

Core techniques include:

- Network scanning and enumeration

- Web application testing (SQL injection, XSS, authentication bypass)

- Social engineering (phishing, vishing)

- API security testing against the OWASP API Top 10

- Privilege escalation and lateral movement testing across internal systems