Yet many fintech companies still approach security testing the way a general enterprise would: periodic vulnerability scans, checkbox compliance reviews, and little consideration of what an attacker could actually do with a misconfigured payment API or a broken authorization flow.

This guide covers what fintech-specific penetration testing actually involves, which attack surfaces it targets, how the process works, what each major compliance framework requires, and how to evaluate whether a testing provider is genuinely equipped for fintech environments.

Key Takeaways

- Fintech platforms face a uniquely high threat profile, combining real-time transactions, sensitive financial data, and complex third-party integrations.

- Effective fintech pen testing targets payment logic, API authorization, cloud infrastructure, and compliance-scoped environments beyond common CVEs.

- PCI DSS, NYDFS 23 NYCRR 500, and GLBA all mandate penetration testing for covered entities; SOC 2 strongly expects it.

- Provider selection hinges on fintech-specific methodology, compliance mapping capability, and post-engagement remediation support.

Why FinTech Companies Face Unique Cybersecurity Risks

An Unusually Broad Attack Surface

Fintech platforms don't have a defined perimeter; they have a collection of surfaces, each handling live financial data simultaneously:

- Customer-facing mobile apps

- Public REST APIs

- Cloud microservices

- Third-party payment processor integrations

- Banking rail connections

- KYC vendor pipelines

Each carries distinct risk. A mobile app might store session tokens insecurely. An API might lack proper object-level authorization. A cloud storage bucket might be publicly accessible. Any single misconfiguration can sit directly between an attacker and thousands of customer accounts.

The Threat Actor Landscape

The actors targeting fintech range from opportunistic cybercriminals to sophisticated nation-state groups. The 2025 DBIR puts it plainly for the financial and insurance sector:

- 78% of breaches involved external actors

- 90% were financially motivated

- 12% had espionage motives, more than double the prior reporting period

The financial stakes are equally stark. IBM's 2025 Cost of a Data Breach report places the average financial industry breach cost at $5.56 million, well above the global cross-industry average of $4.44 million. Ransomware, credential theft, and business logic exploitation are the dominant attack patterns, not zero-days.

Third-Party and Supply Chain Risk

Fintech platforms rarely operate in isolation. They integrate with banks, payment networks, identity verification vendors, fraud detection engines, and data aggregators. Every integration is a potential entry point.

Supply chain compromises now account for 15% of all breaches globally, with an average cost of $4.91 million and a detection-and-containment window averaging 267 days. For fintech, where vendor integrations are core to product functionality, supply chain exposure is a first-order pen testing concern, not a secondary one.

What Does FinTech Penetration Testing Actually Cover?

Fintech pen testing is not a one-size-fits-all exercise. Scope must align to the specific assets and financial workflows that carry real business risk. Testing typically spans four surfaces.

Web Applications and Mobile Apps

Web and mobile apps are the primary entry points attackers use to pursue unauthorized account access, transaction manipulation, and data theft. Testing these surfaces should cover:

- Broken or bypassable authentication mechanisms

- Insecure session management and token handling

- Improper authorization allowing access to other users' data

- Insecure local data storage in mobile apps

- Input validation gaps that enable injection or business logic abuse

Methodology should align to OWASP Top 10 for web applications and OWASP MASVS for mobile, used as a framework for what actually matters in financial contexts, not just ticked off as a compliance checklist.

APIs and Payment System Logic

APIs are the highest-risk surface in modern fintech. They connect banking systems, payment processors, fraud engines, and customer-facing applications into a single functioning platform.

According to Akamai's API Security Impact Study, 88.7% of financial services companies experienced an API attack in the prior year, with an average financial impact 40% higher than the cross-industry mean.

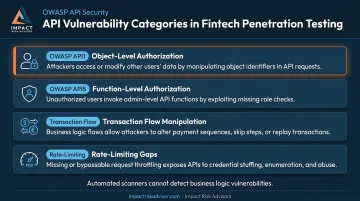

What separates fintech API testing from generic endpoint scanning is active testing of:

- Object-level authorization (OWASP API1): can one user access another's account data by changing an ID parameter?

- Function-level authorization (OWASP API5): can a standard user invoke admin-only operations?

- Transaction flow manipulation: can an attacker alter payment amounts, duplicate transactions, or exploit refund logic?

- Rate-limiting gaps: are brute-force and enumeration attacks adequately throttled?

These are business logic vulnerabilities. No automated scanner will surface them; they require a tester who understands how payment flows are supposed to work and knows where to apply pressure when they don't.

Cloud Infrastructure and Data Storage

Fintech workloads increasingly run on AWS, Azure, or GCP. Cloud-specific risks that pen testing must validate include:

- Publicly exposed storage buckets containing customer financial data

- Overly permissive IAM roles that allow privilege escalation

- Weak or absent encryption for data at rest and in transit

- Insecure Kubernetes configurations in containerized environments

The goal isn't to run configuration benchmarks; it's to validate whether a real attacker could chain these misconfigurations into access to sensitive financial data.

Network Segmentation and Internal Infrastructure

PCI DSS requires organizations to prove their cardholder data environment (CDE) is isolated from the rest of the network. Pen testing validates this through lateral movement simulation, confirming that an attacker who gains initial access to a lower-trust environment cannot pivot into payment infrastructure.

This isn't optional. If lateral movement testing reveals a path from a compromised workstation to cardholder data, that's a finding your QSA will require you to remediate before your assessment closes.

How FinTech Penetration Testing Works: The Process Step by Step

Planning and Scoping

Scoping is where fintech engagements differ from standard pen tests. Testing live payment systems requires careful coordination to avoid disrupting production transactions. This phase establishes:

- Test type: black box (no prior knowledge), gray box (partial knowledge, most common for fintech), or white box (full architecture access)

- Scope definition: which assets, environments, user roles, and API endpoints are in scope

- Rules of engagement: what actions are permitted, time windows, escalation contacts

- Compliance objectives: whether the test must generate PCI DSS segmentation evidence, SOC 2 audit documentation, or NYDFS-compliant testing records

Getting scoping right determines whether the test generates genuine security and compliance value.

Reconnaissance and Discovery

Before exploiting anything, testers map the full attack surface: exposed endpoints, API documentation and versioning, authentication flows, third-party integration touchpoints, and cloud asset inventory. In fintech, this phase specifically includes mapping transaction flows and understanding business logic because exploiting payment systems requires understanding how they're supposed to work first.

Exploitation and Attack Simulation

This is where fintech pen testing separates itself most sharply from standard assessments. Testers don't just confirm vulnerabilities exist; they actively exploit them, chain multiple weaknesses together, and simulate realistic attacker behavior.

Consider what happened with Fiserv's online banking platform in 2018. A flaw allowed attackers to access other customers' account alerts (including email addresses, phone numbers, and full account numbers) simply by manipulating a sequential event number in the site's code. The platform served approximately 1,700 banks.

No CVE. No unpatched software. A pure access-control logic failure that automated scanning would never have flagged.

This is why manual expertise is non-negotiable in fintech pen testing.

Reporting and Remediation Guidance

A high-quality fintech pen test report includes:

- Findings prioritized by business impact, not just CVSS scores

- Proof-of-concept details showing exactly how each finding was exploited

- Compliance mapping: which PCI DSS requirement, SOC 2 criterion, or NYDFS section is affected

- Actionable remediation guidance that engineering teams can implement without translation

The report that satisfies a compliance auditor is different from the one a developer needs to fix a vulnerability. Impact Risk Advisors structures pen test deliverables to generate compliance-ready evidence that feeds directly into audit packages, reducing the documentation burden on internal teams.

Retesting and Validation

The engagement doesn't end at report delivery. After engineering remediates findings, a retest confirms that vulnerabilities are fully resolved and no new weaknesses surfaced in the process.

Skipping retesting is a common and costly mistake. The original test only generates value when the vulnerabilities it finds are actually fixed.

FinTech Pen Testing and Compliance: What Each Framework Requires

For fintech companies, regulatory compliance isn't a soft motivator for pen testing; it's frequently a contractual or legal obligation. The four frameworks US fintech companies most commonly encounter are PCI DSS, SOC 2, NYDFS 23 NYCRR 500, and GLBA/FFIEC.

PCI DSS 4.0

PCI DSS v4.0 is explicit. Requirements 11.4.2 and 11.4.3 mandate internal and external penetration testing at least annually and after any significant infrastructure or application change. Key obligations include:

| Requirement | What It Mandates |

|---|---|

| 11.4.1 | Documented pen testing methodology covering the CDE perimeter |

| 11.4.2 / 11.4.3 | Annual internal and external testing; after significant changes |

| 11.4.4 | Exploitable findings must be remediated and retested |

| 11.4.5 | Segmentation controls tested annually |

| 11.4.6 | Service providers must test segmentation every 6 months |

Test results and remediation documentation must be retained for at least 12 months for auditors.

SOC 2

SOC 2 doesn't mandate penetration testing by name. However, pen test reports are widely expected as evidence under:

- CC6 (Logical and Physical Access): demonstrating that access controls work as intended

- CC7 (System Operations): supporting vulnerability identification and monitoring controls

Enterprise customers increasingly require SOC 2 pen test evidence during vendor due diligence. Fintech companies selling to larger institutions that skip pen testing frequently hit friction in procurement.

NYDFS Cybersecurity Regulation (23 NYCRR 500)

New York's NYDFS regulation requires covered entities to conduct annual penetration testing and biannual vulnerability assessments (absent effective continuous monitoring). Key obligations include:

- Annual pen testing and biannual vulnerability assessments

- Section 500.17(b) annual written certification of compliance to the Superintendent

- Coverage extends to money transmitters, BitLicense holders, and banking charter holders

This applies to any entity operating under a New York Banking Law, Insurance Law, or Financial Services Law authorization. Fintech companies holding relevant New York licenses must treat NYDFS pen testing requirements as mandatory.

GLBA / FFIEC

The FTC's GLBA Safeguards Rule (16 CFR Part 314) requires covered financial institutions to conduct annual penetration testing and vulnerability assessments at least every six months, including when material changes occur. Results must be reported annually to the board or governing body.

FFIEC guidance applies to bank-affiliated and institution-aligned fintech environments, requiring pen testing frequency and scope to reflect the institution's risk assessment.

What to Look for in a FinTech Penetration Testing Partner

Providers who primarily run automated scans or lack financial-sector experience will miss the logic-level vulnerabilities that pose the greatest actual risk. The right partner brings three capabilities that most generalist firms don't:

- Transaction-level coverage: testing scopes include transaction flows, API authorization logic, and payment system business logic, not just OWASP Top 10 checkbox items

- Audit-ready reporting: findings map directly to PCI DSS requirements, SOC 2 criteria, or NYDFS obligations so they can be used in audits without additional translation work

- Remediation follow-through: retesting and validation are built into the engagement scope, not billed separately after the fact

Point-in-Time vs. Continuous Testing

Annual point-in-time tests leave significant windows of exposure for fintech teams deploying code frequently. A vulnerability introduced in a March release won't be caught until the following January.

PTaaS (Penetration Testing as a Service) models address this by providing on-demand or continuous testing aligned to development and release cycles. As providers like Synack describe it, PTaaS combines automation with human expertise for ongoing coverage, rather than a single annual snapshot.

For fast-moving fintech teams, continuous or quarterly testing aligned to deployment cadence is increasingly the practical standard, not the premium option.

Impact Risk Advisors' Approach

That continuous model is exactly how Impact Risk Advisors is structured. Rather than isolated engagements, the firm provides embedded, ongoing support, which means findings connect directly to the client's broader security posture and compliance program, not just a standalone report.

The practical outcomes: reduced cyber insurance premiums through demonstrated risk management maturity, stronger customer trust, and the ability to share credible security evidence with enterprise prospects and auditors during procurement.

Frequently Asked Questions

What are the three types of penetration tests?

The three types map to how much information testers receive upfront:

- Black box: No prior knowledge of the system, simulating an external attacker

- Gray box: Partial knowledge, simulating a compromised insider or third-party vendor, and the most common approach for fintech engagements

- White box: Full architecture and code access, maximizing coverage for complex environments

How much does a pentest usually cost?

Costs typically range from $10,000 to $150,000+ depending on asset complexity, test type, cloud environment scope, and compliance requirements. The cheapest options are usually automated-scan-heavy engagements with minimal manual testing, a poor fit for fintech's logic-heavy, API-dependent risk profile.

What is cybersecurity in fintech?

Cybersecurity in fintech refers to the practices, technologies, and controls that protect financial platforms, customer data, and transaction systems from cyber threats. This includes encryption, access controls, fraud detection, penetration testing, and compliance with frameworks like PCI DSS, SOC 2, and NYDFS 23 NYCRR 500.

How often should fintech companies conduct penetration testing?

At minimum annually; PCI DSS also requires testing after significant infrastructure changes. Fast-moving fintechs should consider quarterly or continuous testing models so new code and integrations don't introduce exploitable gaps between annual assessments.

What compliance frameworks require penetration testing for fintech?

The key frameworks requiring or strongly recommending penetration testing include:

- PCI DSS: mandatory for cardholder data environments

- NYDFS 23 NYCRR 500: mandatory for covered entities

- GLBA Safeguards Rule: mandatory for covered financial institutions

- SOC 2: strongly recommended as audit evidence for CC6 and CC7 controls

How is fintech penetration testing different from a vulnerability scan?

Vulnerability scans are automated tools that identify known weaknesses in software and configurations. Penetration testing involves human testers actively exploiting those weaknesses, including payment logic abuse, API authorization bypass, and transaction manipulation, that automated tools cannot detect or simulate.